How Credit Management is the Key to new Business Financial Stability

It is indeed hard for any new entity to set a mark in today’s business, when it has many challenges. Everything from market competition, to operational roadblocks can threaten your path to success. And perhaps, one of the most important aspects to ensuring long-term success is achieving financial sustainability. So, what is the magical potion that can either be a benefit or bane for any new business when it comes to finances? This reason is simple: efficient credit management.

That being the case, here we go for startup founders or those interested in growing their small business with a financially get foundation on how to buckle up and take off. But that’s about to change as we show the secrets of a vital, and often overlooked aspect of business finance: credit management.

How Credit Management can be Handled for New Businesses

Past the basics, for a new business, credit is necessary and can heavily impact all aspects of your company. It is essential for a business to have an effective credit management process in place as it forms the base of any organization that wants to be strong, resilient and growth oriented.

Establishing a robust base of credit in the beginning ensures new businesses lay a foundation for financial stability, strategic growth, and long-term success. It turns credit management from being a rationotal support function into something that is key to the business strategy, worth creation.

Financial Stability

Every Dollar Matters When You Start A Business Just as with a financial safety net, effective credit management will allow you to catch yourself before hitting the floor. This is a way to balance cash flow and reduce risk of financial hiccups. How? Preventing delays in payments

Think about it: eliminates bad debt good credit management. That is a major injection to your income and financial confidence. Think of all the work your business could do with that money: grow, offset a surprise payment or just relief yourself of having to live life on shaky financial ground.

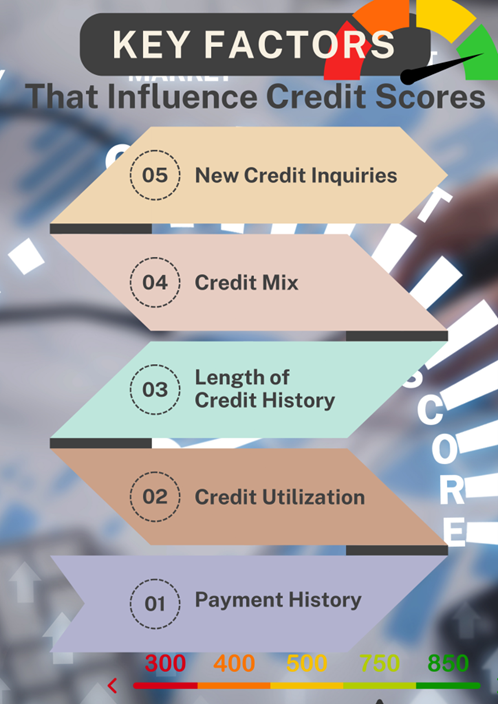

An effective credit management process allows your business to develop and maintain a healthy credit score, needed fast capitalization with loans or better terms on payables from suppliers. For instance, addressing problems such as a Midland Credit Management lawsuit quickly can prevent even worse financial fallout and safeguard the commercial reputation of your business.

Midland credit management problems or Midland Funding LLC complaints have the ability to do damage to a business’ when you really think about it credibility, and stability. Furthermore, any ongoing midland funding lawsuit can also create complications,which is why it is important for start-up businesses to take preventative measures concerning their credit.

Business Reputation

When you’re a new entrepreneur (and even an old one,) social proof is gold. Now you might have heard that suppliers are coureous of giving any business credit unless they got their account information to hand. You guessed it — your supplier relationships can hinge on where you fall with respect to credit.

How good reputation with a credit line may open the doors. It projects stability, confidence to both your suppliers and customers. In the business, this reputation can be a competitive edge separating you from million others.

Best Practices in Credit Management

Credit management, as we have seen is not all about numbers but building a sturdy base for our business. But, what is indeed effective credit management and how do you get to put it into practice? In this post, we are gonna dive thorough into the core practices that can help achieve these gains and keep above them.

FlippingMastery understands well that there are two very important components for a bank to play into the service and those are risk assessment and credit scoring.

This means thinking of risk assessment as the financial radar for your business. It allows you to identify incoming storms in their infancy. You need to look at the financial well-being of your clients and determine whether they are credit-worthy on a regular basis. It is as though you have a crystal ball that will tell you who is likely to pay on time and who may not be helpful.

Regular credit assessments can be used to reduce the default risk. And that is a considerable buffer to insulate your business’s financial well-being. Understand the Risks — Save Your Capital One of the biggest risks when making a loan is your own loans may not be repaid.

Credit Terms and Conditions

The credit policies that are well defined, personalized work as if it were the rule of the game. They let everyone know what they can expect and how to be a good sport. Not only are you creating policy, but a blueprint for the best financial predictability and boundaries.

The impact? When there is confusion with credit policies, payment collection rates go down and companies can play recovery remove the problems. Faster money in the bank. On top of that, it creates good relations with clients (in fact any client appreciates some indication where stands).

Non-Monetary Benefits

Reaping these benefits at scale to remain on par with today’s business circumstances necessitates the implementation of ultramodern technology in credit management operations. In this post, we will be learning about how technology is changing credit management.

Customer Relationships

Good credit management is not just about getting the money in – it needs to be done right so customers learn that you can be trusted. Transparency and fairness in your credit practices will help you build positive, long-term relationships.

Consumers are more likely to trust businesses that demonstrate transparency in keeping their data get. This loyalty translates into repeat business, a preference for the restaurant over others in town and lots of positive word-of-mouth—pivotal factors to ensure growth.

Expansion and Opportunities in Business

Efficient credit management not only shields your business, but also pushes it down the highway. You will be in a better position to make the most of new opportunities when your finances are under control. Enterprise said its credit management program has allowed it to seek new business from an acquisition and expansion perspective.

With a proper credit manager, you can make new strategic moves without the fear of running out of money.

Technology in Credit Integration

Codex credit management is about as useful in the virtual time as trying to win a car race on foot. GET THERE FIRST WITH ULTRA-FAST AUTOMATION This leads to lower collection times for businesses that rely on automated credit management. This efficiency gain is not just about time saving it but cash flows, reduced errors and allow your team to focus on growth-oriented tasks.

The real-time monitoring puts your credit file on life support and you can stay alive with it or die without anytime. This serves as a financial distaster prevention tool that allows you to identify potential problems before they happen.

Data Security and Compliance

Since data breaches have become a regular have of our bedrooms and Twitter feeds, keeping financial information safe is no less than the supreme commandment! Compliance is not only a matter of avoiding fines– fundamentally, it seeks to establish trust. Most companies accept the importance of data security in credit management due to the compliance and need for protecting customer personal data.

Ensuring data security within your credit management activities goes past just checking the box but also establishes you as a partner people can trust.

These are the major innovations and have an immediate impact on our operations, which in turn can be replicated to drive sustainable long-term growth. The operational benefit from credit management is clear, but what are the long term strategic implications of good and effective credit?

Strategic implications over the long-term

Proper credit management can be considered as container gardening for the . This builds a solid financial base to continue supporting the business as it scales.

Companies with disciplined credit management are in a better position to realize sustainable growth and scalability throughout their business(sf). It cements the pivotal of credit management in everyday business and changes it made to the when you really think about it Business.

Credit Management for the

There is growing excitement for the of credit management, as newer technologies introduce more efficiencies and insights. AI technology for credit management will improve efficiency and strengthen predictive analytics to better inform decisions.

Just consider: predicting market trends, customer behaviors and financial risks with greater accuracy – This is AI in credit management. These strategic implications signal a bright , but what are some common questions companies usually ask themselves before deciding to adopt such practices?

Conclusion

It is the credit management that ensures your new business remains solvent, so it must be treated as a strategic asset more than just another financial tool. It helps the business grow and is related to every part of your business, stronger foundation ground till opening up doors for growth.

Risk assessment and smart credit policies, technology, the : you’re not managing your company’s financial aspect; you are preparing it for growthAnimationFrame >

After all, your personal credit is still tied to the business in many ways and of course — in business time, your financial reputation (or lack thereof) precedes you. Keep it high and level through shrewd credit management.

FAQs

- Credit Management: The right way to Fuel Business Growth?

Good credit management is a pivotal factor in driving cash flow. This improved cash flow is essential to funding growth initiatives, taking advantage of new opportunities, and overcoming the challenges that come with growing a business.

- So what are the dangers to a new business of poor credit management?

Mismanagement of credit can result in more cash flow problems. This can lead to businesses going under and so damaging supplier relationships, so opportunities for growth are missed. You might as well try to run a marathon tomorrow without ever having trained once — you’re not giving yourself the proper tools for success.

- So how do start-ups, especially when identifying new businesses that can not yet rely on the credit insurance of a receivable provider, go about ensuring they have purchase strategies in place to offer their customers and so themselves best protection.

Start-ups ought to place in credit evaluation models which may help lower the bad debts. The best way to begin is by learning your credit circumstances in the industry, establishing terms and conditions from every possible angle as well as reviewing and updating them regularly. Your credit policy, like your business, should always be gaining and changing.